Brief preview of the upcoming week (CBs, CPIs)

Brief preview of the upcoming week (CBs, CPIs)

The next few days will keep us busy.. maybe

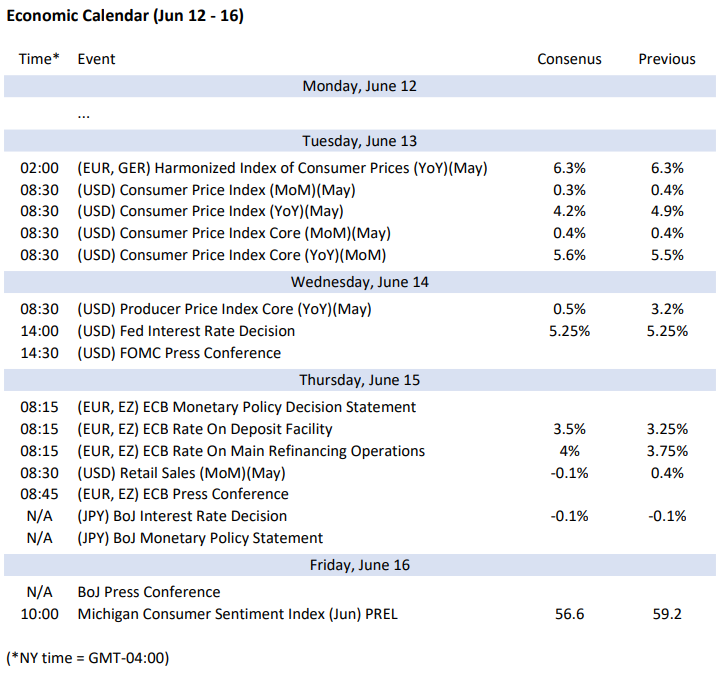

The FX market should await the coming week with great excitement. There are major central bank meetings and important economic data releases on the agenda. The following calendar contains a personal (!) selection of the most important dates:

(source: fxstreet.com, own representation, no responsibility is taken for the correctness of this information)

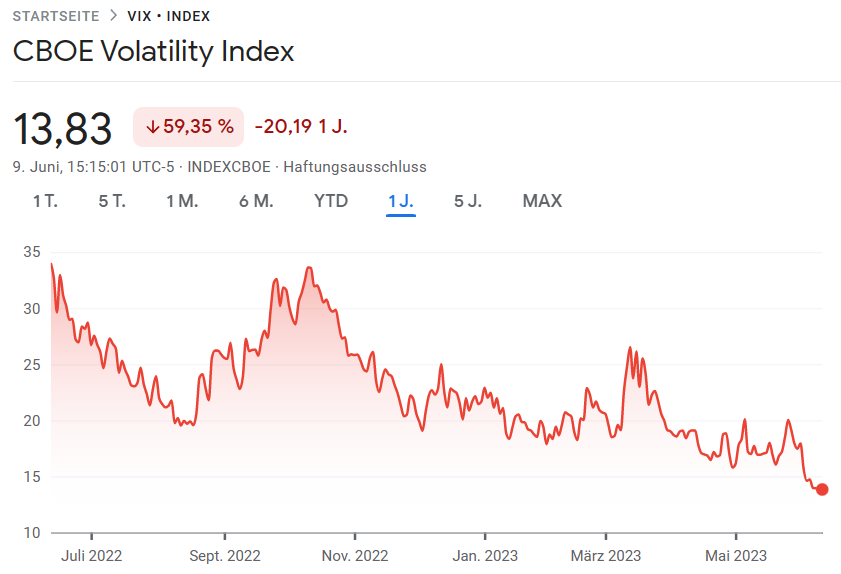

Despite this busy calendar, however, the FX market and capital markets in general seem relatively relaxed. On the one hand, the CBOE Volatility Index (VIX) even fell below the 14% mark last week. These are levels we last saw before the Covid crisis.

(source: google finance)

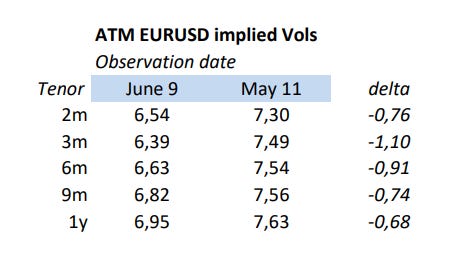

On the other hand, implied EURUSD volatilities have fallen in recent weeks to levels we have not seen since February 2022. That was admittedly very surprising to me, but obviously the market sees far less risk than I do.

(source: cme group, own representation)

The big question, of course, is whether the low volatility environment will continue or whether we will see more of a reassessment of risk. Unfortunately, we won't know the answer to this question until later in the week, maybe even the following week. Personally, I think it is more likely that the risk appetite that has been rising since October 2022 has to undergo a reality check in the coming trading sessions.

Directional trades are subject to a large event risk. In this respect, it makes more sense to turn to the options market. Those who are concerned that the boredom will continue over the summer, but still want to be positioned, should focus on maturities around 6 months. This could bridge the summer without losing too much time value. Risk-taking players may look to the three months to get not only Vega but Gamma in the books.

I wish you a good start to the week!

Sebbo