Current EURUSD Straddle break-evens

1m, 3m, 6m (EUR Calls hedged)

I will keep this post short as it should be self-explanatory along with the market data (prems and deltas* are given by issuer). Of course, the selected retail products do not perfectly match today's OTC expiries. But for the calculations of the forwards I interpolated the points accordingly and you should be able to adapt it well for your own purposes. I will state the respective securities identification numbers (ISIN), but I have absolutely no connection with the issuers.

If you would like, you are welcome to let me know whether you also have access to the selected warrants in your country. I'd be very interested in that.

1mth EURUSD Call (hedged)

ISIN DE000DV5ZZG9 (DZ Bank)

Expiry 30sep22

Strike 1.0000

Spot ref 1.0015

Fwd rate 1.0033

Prem 1.55 (EUR; 10.000 EUR Notional = 155 EUR prem)

Delta 0.5407

3mth EURUSD Call (hedged)

ISIN DE000VV470L1 (Vontobel)

Expiry 02dec22

Strike 1.0100

Spot ref 1.0015

Fwd rate 1.0077

Prem 2.01 (EUR; 10.000 EUR Notional = 201 EUR prem)

Delta 0.4971

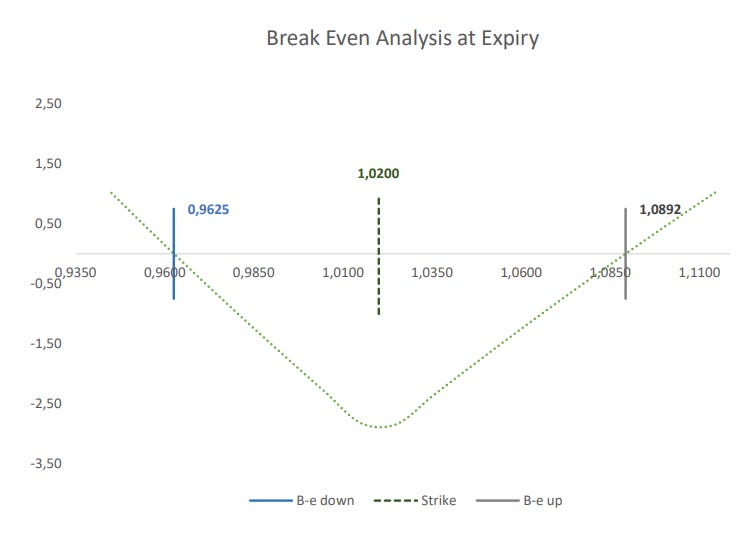

6mth EURUSD Call (hedged)

ISIN DE000PD562K7 (BNP Paribas)

Expiry 17mar23

Strike 1.0200

Spot ref 1.0015

Fwd rate 1.0151

Prem 2.83 (EUR; 10.000 EUR Notional = 283 EUR prem)

Delta 0.5182

As an active trader, I would probably opt for the 3 months expiry. With this tenor you have both, gamma and vega, and you can try to maximise your profits by delta hedging. With a real need for hedging, the 6 months would probably be more interesting. The 6m ATM implied Volatility is still supported above the 10% lvl. That is a bit higher for the recent past, but the times of low inflation and accommodative central banks are obviously over.

Good luck,

Sebbo

(*the reported delta does not always look consistent, but small deviations are not a big problem in the calculation -- reminder: my content is intended to be used and must be used for informational purposes only. It is very important to do your own analysis before making any investment based on your own personal circumstances.)