Market update #14

The Euro is also trading firmly against the Dollar in the new year, but this is not particularly reflected in the implied volatilities. Compared to the last update (see #13), the Euro is about two big figures higher, but especially implied atm vols between 2 months and one year are not much lower. The comparison of the shorter maturities is a bit more difficult, as they mainly covered the public holidays at the last observation time (21dec). The volatilities of the low delta puts, on the other hand, have softened a little more.

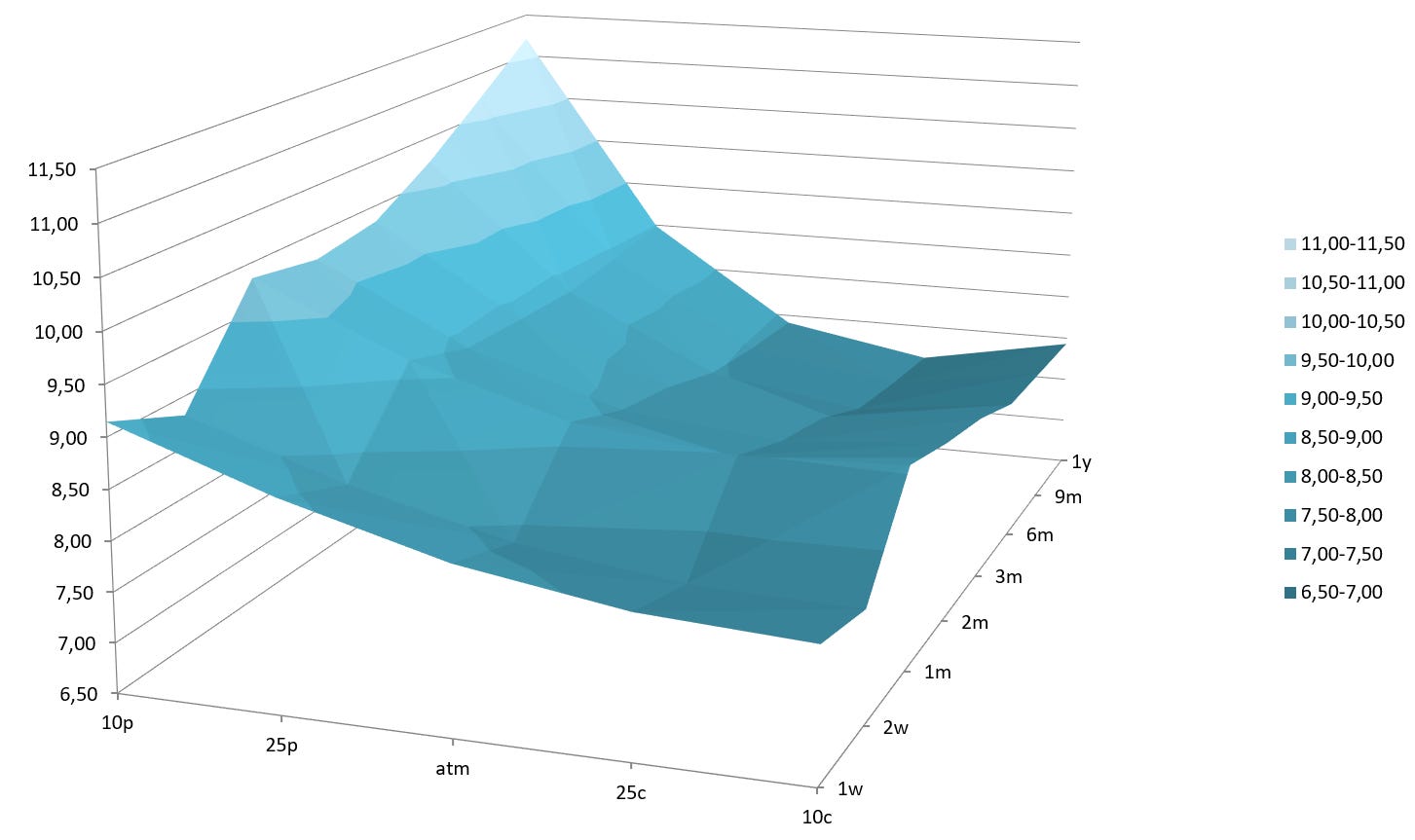

The following vol table shows the quotes at 06:00 NY time. Please note that I changed the order of the left-to-right sorting (now puts to atm to calls). This order makes more sense, even if nothing changes in terms of content. Of course, this also changes the volatility surface graphic.

(source: cme group, own representation)

The lower delta put prems show that the market is pricing some risk out of the euro. For example, while the 25 delta puts in the tenors 2m to 1y are quoted between 0.5% and 0.6% lower, the 10 delta puts are already trading between 0.7% and 1.15% lower. In contrast, the implied atm volatilities, which have hardly changed, indicate that a higher spot rate does not automatically lead to lower atm vols. Consequently, the demand for optional hedging could also increase to the upside.

(source: data from table, own representation)

The volatility skew still favors low delta puts but at a slightly lower level. The market therefore still sees the risk clearly on the downside. What is particularly striking in the volatility surface is the jump from the 2-week term to the monthly term. The latter includes the ECB's next interest rate meeting on February 2nd and a larger rate hike could of course affect the spot rate (see G10 Central Bank Calendar).

In summary, it can be stated that higher euro spot rates are slowly moving into the focus of the options market. After all, hedging is cheaper (for delta < 0.5) for dollar buyers and I also recommend using a higher euro to buy downside protection. Anyone who reads my FX newsletter regularly knows that I have my eyes on the 1.10/1.12 mark. In the medium and long term, however, I believe that we will see the lows of 2022 again.*

Good luck,

Sebbo

(*reminder: my content is intended to be used and must be used for informational purposes only. It is very important to do your own analysis before making any investment based on your own personal circumstances.)