Market update #18

The euro is off the highs (annual high 18 July was 1.1275) and is now trading around the level of the last Market update (05 Jul). This means that the July rally has been completely reversed. Of course, the euro could be supported again here in the short term. But the disappointment over yesterday's FED minutes, which gave no indication of imminent rate cuts, could linger a little longer.

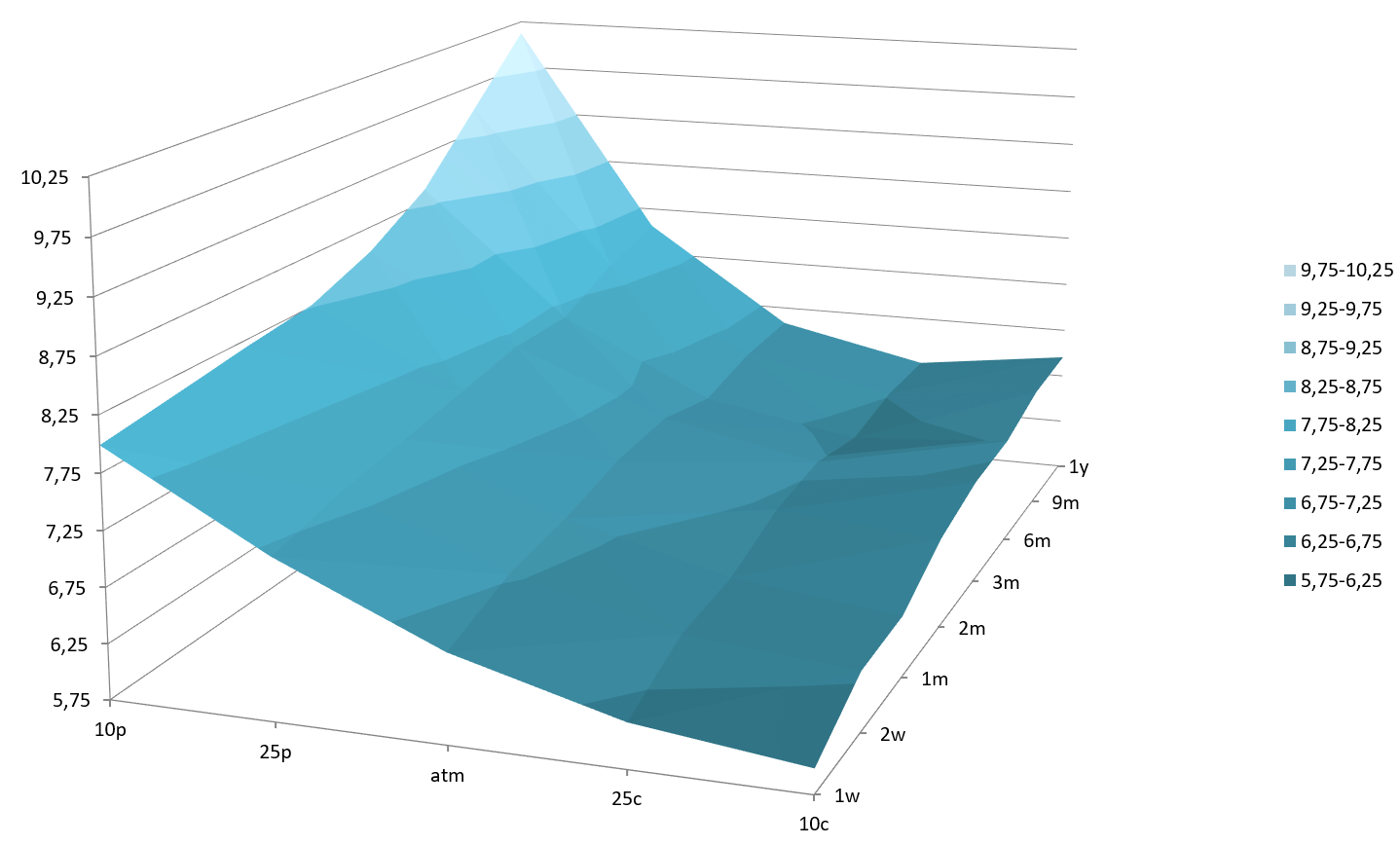

The FX options market shows, first, that we may have already seen the lowest implied volatilities this year and, second, a rebound in downside risk to the euro.

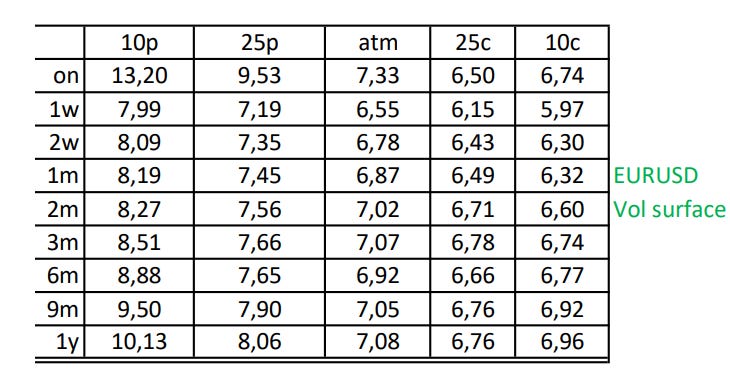

(source: cme group, own representation)

The upper table shows quotes of EURUSD impl Vols at 07:40 NY time. The extremely low impl Vols that we observed in the last Market update have thus been partially corrected. Overall, however, the situation on the FX options market is still quite relaxed. The 6-month ATM vol is still trading below 7%, which is remarkable.

There was a little more movement in the low delta puts, which increased significantly by up to 0.75 percentage points. The low delta calls, on the other hand, only gained about 0.45 percentage points. Particularly noticeable is the 1-year tenor for 10 delta puts, which is now quoted above 10% again. The skew favoring puts also becomes clear in the following graph:

The skew to the dollar call (euro put) side has become even more extreme compared to the last observation period (at the same spot level!). The options market thus sees an increasing risk to the downside in the EURUSD exchange rate. From the perspective of a protagonist with a real hedging need (dollar buyer), 6mth ATM options are currently probably the tool of choice. The strike should be around 1.1000 (fwd points today 102), covering the upper end of the EURUSD trading range of the past 18 months.*

Good luck

Sebbo

(*reminder: my content is intended to be used and must be used for informational purposes only. It is very important to do your own analysis before making any investment based on your own personal circumstances.)