Market update #6

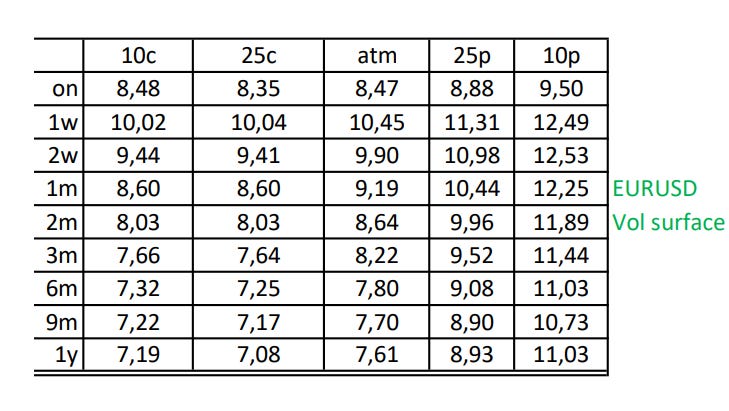

The market has obviously gotten used to the war, the main event of this week (FED) is behind us and EURUSD has recovered from the lows. All of that was enough to bring the implied Vols down. Compared to the last update tenors with vega exposure from 3m to 1y have dropped by 0.75% to 1.25%. Short-dated FX options, of course, have fallen even further by 1.50% to 2.00%.

(source: cme group, own representation)

As I had already written in the Morning Call #63, the market still has to deal with reality. This applies to both monetary policy of the FED and the Ukraine-Russia conflict. The FED is a least one step ahead of the ECB and has finally started to reduce their balance sheet and hiked the key interest rate by 25 bp on wednesday. This should initially support the Dollar in the medium term, even if expectations for the Fed beyond 2022 are not very high.

I'm not an expert on geopolitics, but I don't think the Ukraine-Russia conflict will be resolved as easily as people would naturally like. Even if Ukraine remains neutral with regard to the NATO, Putin is unlikely to be satisfied. All the “effort” just to keep Ukraine out of the NATO? Unfortunately, I think it's more likely that he wants the whole country, including the valuable wheat fields.

Either way, there is little reason to expect much lower Vol levels for now in my opinion. The 7% mark has been an important resistance and I recommend to buy optionality above this level. Of course, things can also develop positively, and of course I hope so too, but assuming that inflation will just die out and central banks can even cut interest rates again when the economy slows down might be a mistake. And this has nothing to do with the Ukraine, but with the general tendency towards de-globalization.

Have a nice weekend!

Sebbo