Market update #8

The current risk situation

The appetite for risk has massivley declined again since the beginning of April. Fueled by the ongoing Ukraine-Russia conflict (in which Europe and the USA are more and more involved), Inflation is hitting record levels after years of central banks' easy monetary policies having caused it to rise sharply. In this respect, it is not surprising that central banks are slowly starting to raise interest rates. Last week, the Royal Bank of Australia and the Federal Reserve Bank hiked their main policy rate by 0.25% to 0.35% respectively by 0.50% to 1.00%.

// It should also be mentioned at this point that the Norges Bank and the Bank of England left their key interest rates unchanged at 1.00% last week. However, this has led to a decent devaluation of both currencies

In any case, higher interest rates are poison for the markets, which have risen to unprecedented heights due to cheap money. Considering that the cycle of interest rate hikes may have just begun, the markets are getting nervous finally. The S&P 500, for example, has fallen 500 points (alomst 11%) since end of March and only some good bids in the last half hour of trading on Friday saved the index above 4100.

(S&P 500, weekly)

The chart above makes it clear: If the 4100 mark breaks on a weekly base, it is only a matter of time before the 4000 level is tested. And there is still plenty of room below that treshold. I advise optimists to look at the S&P 500 chart since 2009.

The further interest rate prospects should therefore be decisive. As you can see in the chart below, the 10yr Treasury-Yield is approaching the important 3.25% mark swiftly. Should this level break -- watch US CPI numbers next Wednesday carefully --, risk sentiment of the markets is likely to deteriorate further.

(Treasury Yield 10 Years, monthly)

(source: yahoo finance)

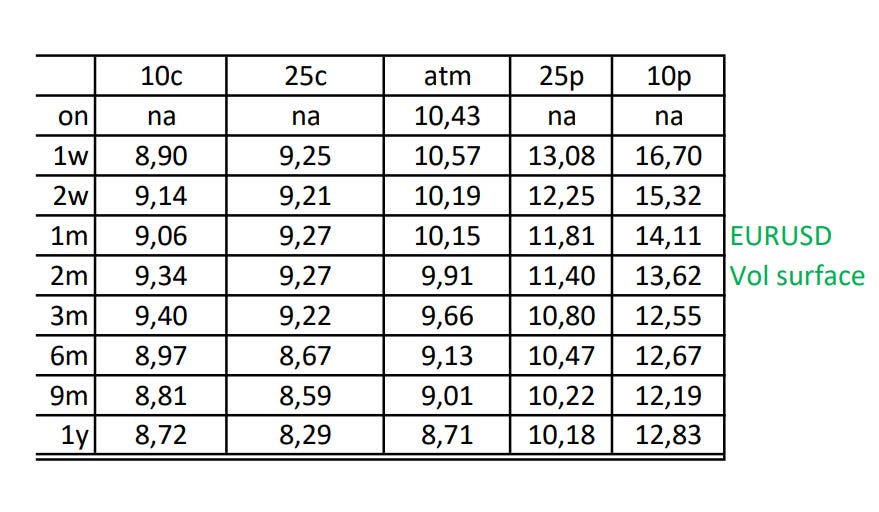

EURUSD implied Volatility surface

Pushed by safe-haven bids and rising rates prospects the Dollar is trading at record highs. The 103.82 and 104.00 together form the last resistance zone which could stop the further rise of the Dollar Index. In this bullish environment (even the safe-haven currencies CHF und JPY are trading weak -- probably mainly driven by relative interest rates prospects), it is surprising that the Euro is not yet trading lower.

(Dollar Index Spot, monthly)

(EURUSD spot rate, monthly)

The currency pair has managed to close above the 1.05 mark every day for the past two weeks, albeit just barely. To that extent I see two-way risks for EURUSD and implied Vols in the next sessions. If the Euro falls below the 1.05 support against the Dollar, it should go down another notch. In this risk off scenario the Euro has to face the prospect of parity if the 1.0340 support will break either. Vice versa there is a chance that the 1.05 has held for the time being.

(source: cme group, own representation)

Implied Vols should also be subject to a greater risk in this respect. Should the Euro continue to fall, the 3 mth to 1 yr tenors with vega exposure will very likely rise above the 10% level. On the other hand, a calming down of the markets and a higher EURUSD spot rate should lead to falling vols again. In particular short-term tenors up to 2 mth should get cheaper.

Of course, I do not know what will happen in the coming days and weeks. But I am afraid we have not seen the worst in the medium term. To that extent I would prefer to buy volatility on a larger dip (0.75% to 1.50% lower) and can only recommend to monitor tactical Euro longs closely. The same applies for risk assets in general. There is a chance for recovery when the outlook for inflation and eventually interest rates calms down. But in the medium term I do not believe in a sustainable recovery for the time being.

Have a nice weekend,

Sebbo