Morning Call #180

Morning Call #180

Jerome Powell caught between rising US deficit and solid figures?

FOMC

So tonight is the next interest rate meeting of the FED. The main focus of market participants will be on the Federal Reserve's dot plot, which implied 75 basis points of rate cuts for 2024 at the last Meeting. Interestingly, the bond market had priced in more interest rate cuts in the meantime, but this has recently been reversed to some extent. As a result, the dollar has made slight gains again in the past trading days. After the first consolidation phase in the first two weeks of January ended with an upward breakout, the dollar index (=DXY) is now once again in an upward (?) consolidation pattern.

Technical view

From a pure chart perspective, another upward attempt could materialise tonight, similar to the one in mid-January. The target of this move could then be the 104.20/40 resistance zone, which also represents the upper side of the 100.80/104.30 range that has been in place since April 2023. This level should ultimately decide whether the dollar can continue to rise in the medium term. Should the FED surprise on the dovish side tonight, however, it will be difficult for dollar bulls below the 102.75 mark. The momentum that has prevailed since the beginning of the year would then finally be over.

")

Macroeconomic view

As I have already indicated above, I believe that bond yields that price in interest rate cuts of more than 75 basis points for 2024 are a bit odd in view of the most recently published economic data and geopolitical developments:

The above table is admittedly a personal selection. The somewhat weaker figures in the Producer Price Index (YoY 1% vs. 1.3% exp) from January 12 must also be pointed out. Overall, however, the picture of a US economy characterized by persistent inflation and solid economic indicators remains valid. To what extent the Fed should lower interest rates beyond its december dot plot in this environment is beyond me. In this respect, a dovish surprise tonight would be a gift to the market, especially to banks and the US Treasury (which has to refinance its massively rising deficit), but it would have little to do with economic reality.

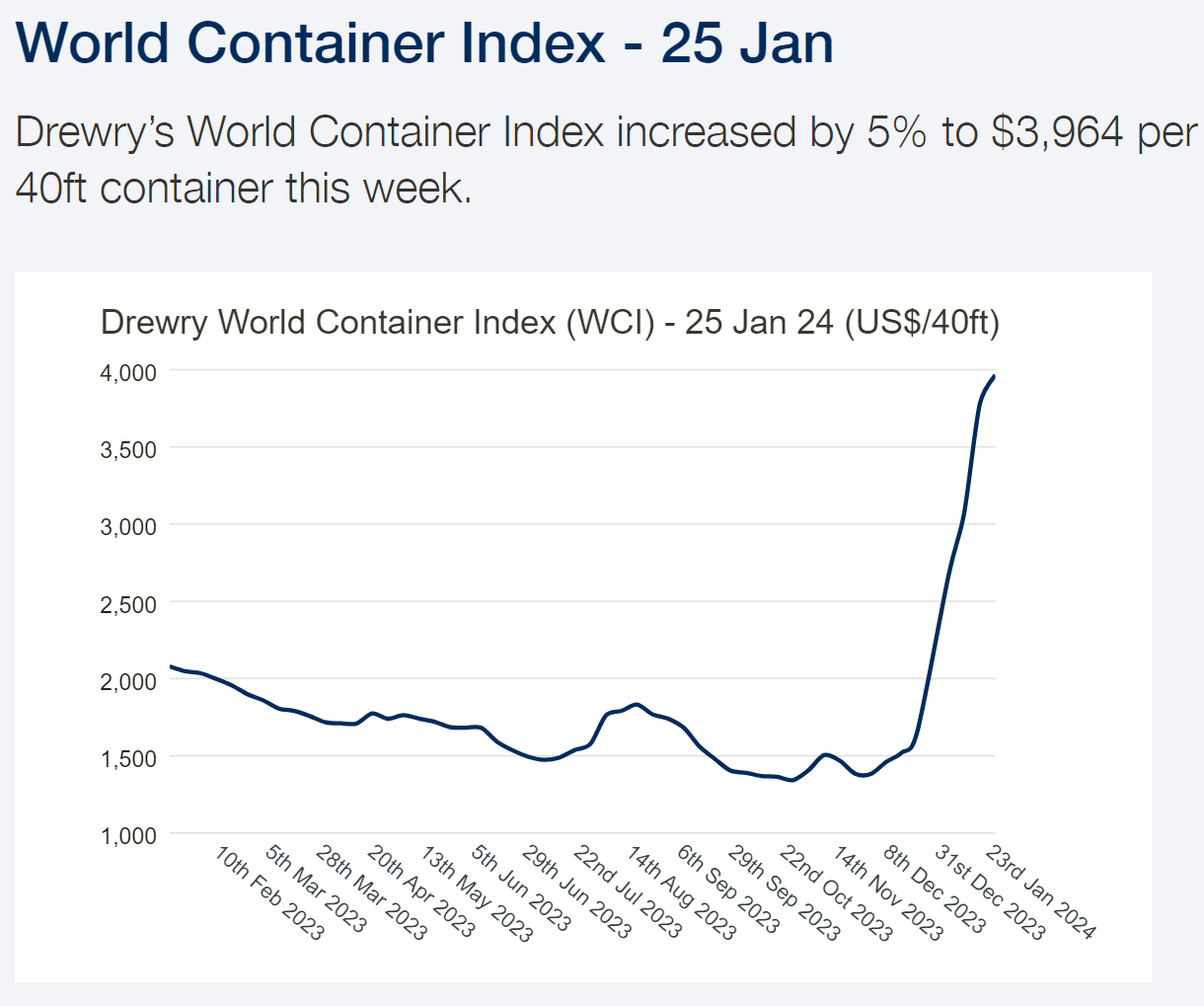

On the geopolitical side, there are also developments that could have an inflationary effect in the short to medium term. Since the end of December, transportation costs for a 40ft container have risen by 238% due to the crisis in the Red Sea (Huthi rebels). This means that the highs of the coronavirus crisis are still a long way off, but vulnerable supply chains will be reflected in prices after all. In any case, they do not have a deflationary effect.

Conclusion

A weaker dollar cannot be deduced from the short-term technical picture and the medium-term macroeconomic view. However, this only applies if the FED does not want to abandon the Taylor rule even further. If US budget policy or the economic constraints of the US banks determine the FED's main focus, the dollar is likely to weaken. I summarised some time ago (MC #168 - 20oct23) that a rapidly rising US deficit would have to be accompanied by rising interest rates. With a FED artificially capping yields, dollar investors may no longer feel sufficiently compensated, which should ultimately lead to a weakening of the dollar.

Directional positioning is naturally difficult with the described two-way risk. In this respect, I would like to refer to the last market update from last Friday. The implied ATM vols are still trading at a low level. In this respect, it may make sense for active players without strong conviction to focus on hedged calls or puts. As the short maturities are of course expensive today, I would personally look at the 3 months.

Good luck,

Sebbo