Brief preview of the upcoming week #2

Brief preview of the upcoming week #2

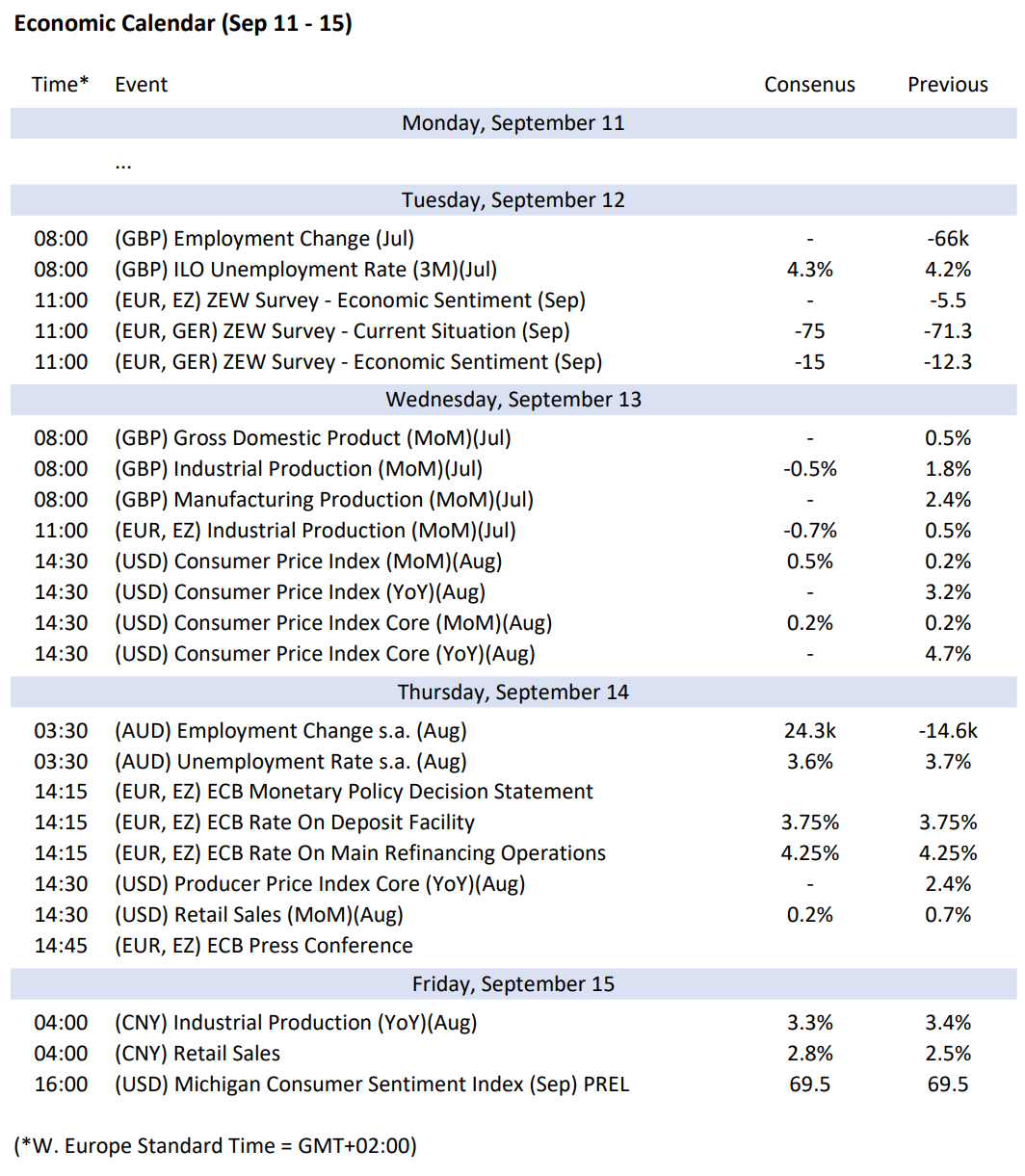

(Sep 11 - 15) US CPIs and ECB Policy Decision

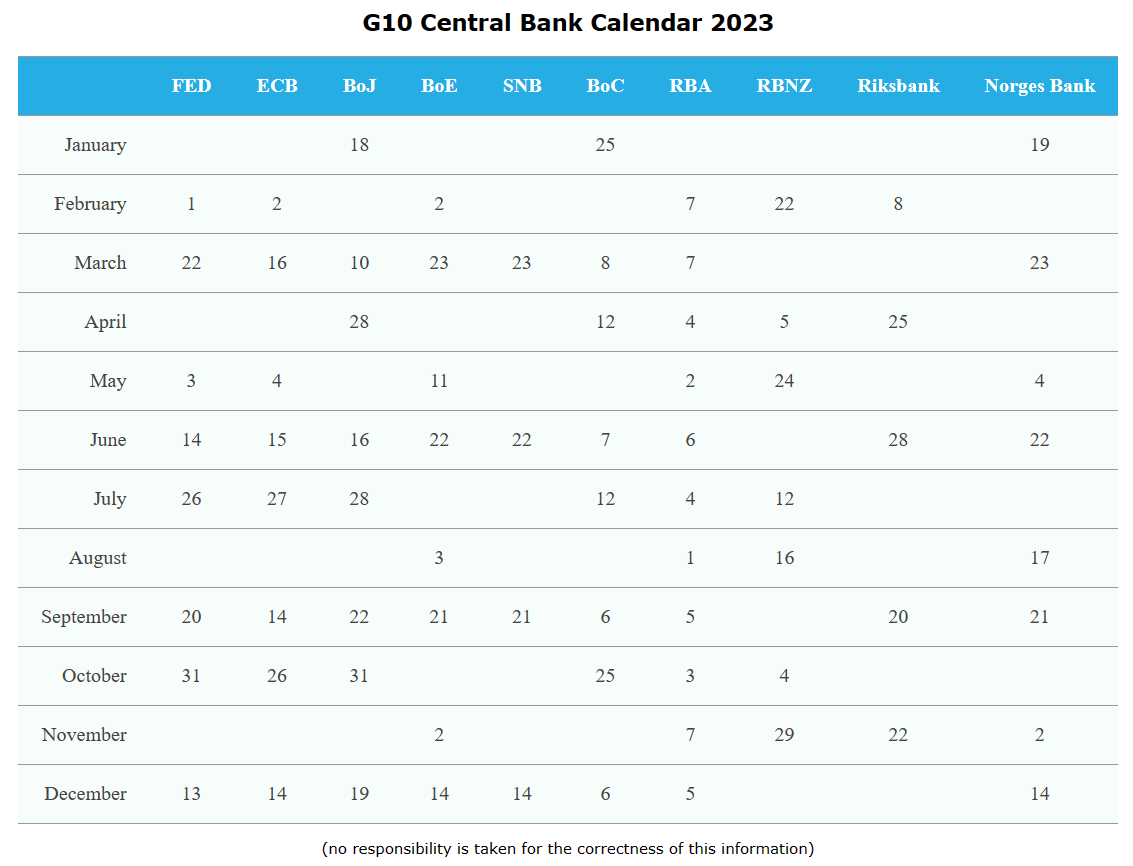

Next week should be interesting again for the FX market. On the one hand, we will see the latest CPI figures from the US on Wednesday. On the other hand, the ECB will be the first of the G10 central banks to decide on its further interest rate policy on Thursday. This will also mark the start of the hot phase of central bank meetings in September, which will become even more exciting the week after next with the interest rate meetings of the FED, Riksbank, BoE, SNB, Norges Bank and BoJ within three days:

(source: fxdesk.de)

In the following calendar I have summarised the most important data releases (personal selection) for the coming week. Please note that individual data points may still change as soon as analysts' estimates are updated:

(source: fxstreet.com, own representation, no responsibility is taken for the correctness of this information)

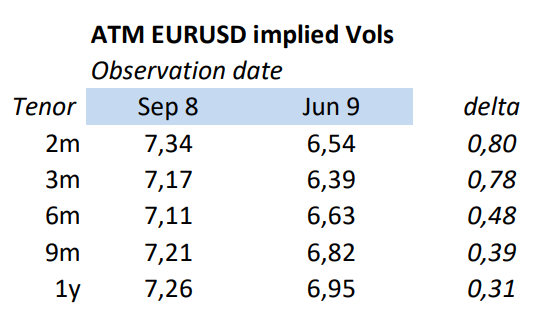

Once again, the market is very relaxed in light of upcoming economic data and central bank meetings. The two risk barometers "CBOE Volatility Index (VIX)" and "ATM EURUSD implied Vols" are still at very low levels. This is somewhat strange in view of a changed interest rate world, central banks reducing their balance sheets and the financial situation of important segments of the population. The VIX is almost exactly at the level of the last preview.

(source: google finance)

The ATM EURUSD implied vols have obviously seen their lows, but the absolute levels are still comparatively low. However, should the EURUSD currency pair exit the 1.0600/1.1000 trading range to the downside, levels just above the 7% will look very favorable in hindsight. Regular readers know that I expect another dip below the 1.0516/1.0483 support zone in the medium to long term.

(source: cme group, own representation)

The overall picture once again shows a market that is not particularly risk averse. To what extent this is justified will possibly become clear in the next two weeks. I state that the above-mentioned indicators do not correctly reflect the market risk at the moment (Inflation, Real wage losses, Private debt, Slump in consumption, High interest burden on government budgets, Rating downgrades). However, this is only my opinion, and as long as the market can negate all risk factors, I will be wrong.

For a positive conclusion, I would like to thank you very much for your subscriptions, likes and comments. Of course, I also write the newsletter for myself to keep track, even in currency pairs that I am not actively trading at the moment. But without your encouragement I would not keep it up. Thank you very much!

Sebbo