Market update #19

Market update #19

A euro recovery could lead to lower impl vols in the short term

The euro is trading about three and a half figures lower against the dollar compared to the last market update. At that time, we had seen the risk on the downside and accordingly recommended a 6-month FX option to protagonists with real dollar needs: “From the perspective of a protagonist with a real hedging need (dollar buyer), 6mth ATM options are currently probably the tool of choice. The strike should be around 1.1000 (fwd points today 102), covering the upper end of the EURUSD trading range of the past 18 months” (Market Update #18). This trade would definitely have paid off and the FX option has only reached a third of its term.

At current spot level the currency pair is trying to form a bottom. In the short-term picture, a countermovement could start here again, which failed at the 1.0635 resistance last week. A recovery could eventually even lead to the 200-day line. With this in mind, it might make sense to think about reducing the delta or selling (partial) the FX option. In the above example of a dollar buyer, the decision naturally also depends on the development of the underlying transaction as to whether an adjustment of the hedge is necessary.

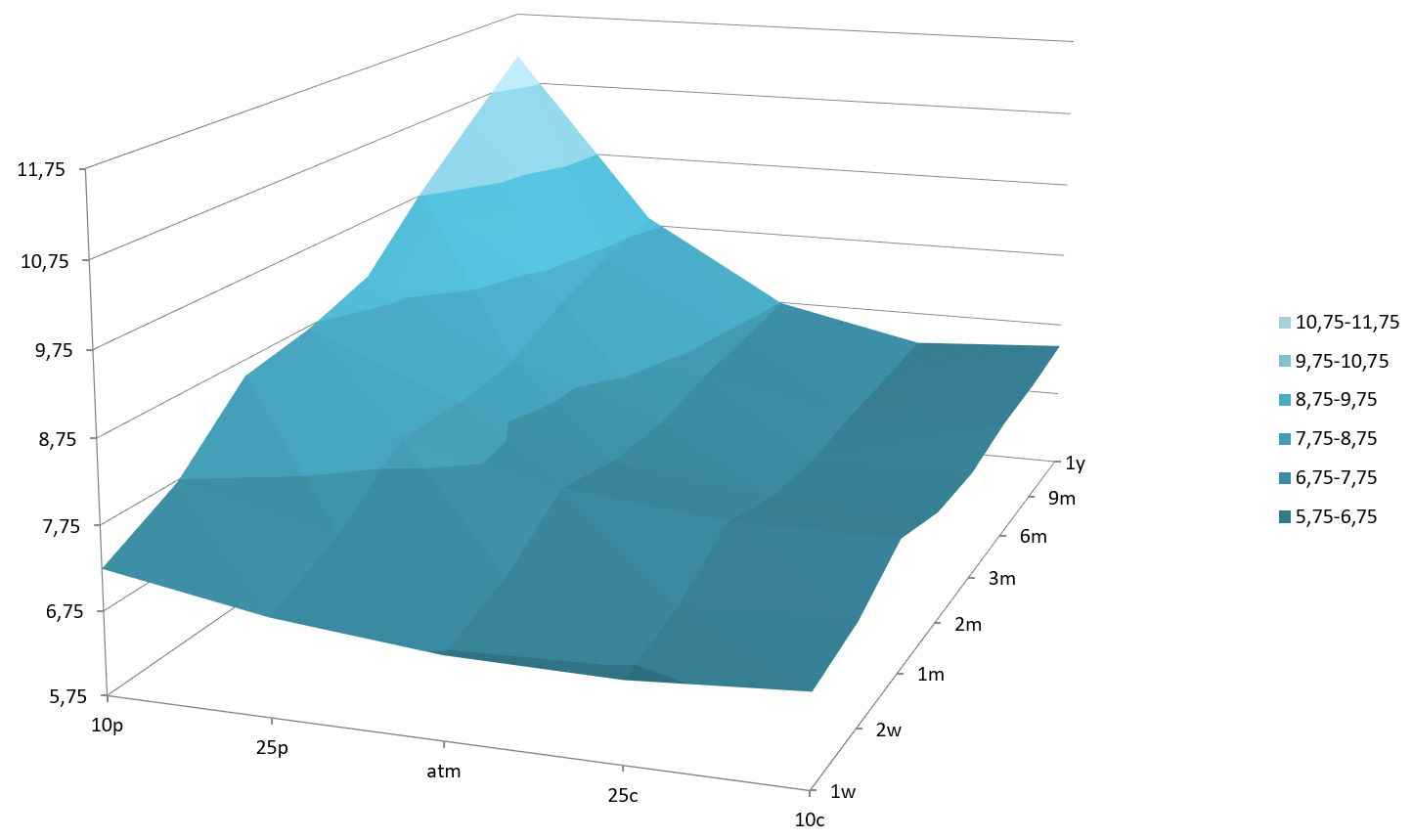

The upper table shows quotes of EURUSD impl Vols at 06:15 NY time. Compared to the last observation date (17 August), implied vols have risen, but even the elevated levels are still quite low at below 8% across all maturities.

In contrast, the 10 delta put implied volatility recorded a larger increase of 1.01%. In the vicinity of the psychologically important 1.0500 mark, this is not particularly surprising. After all, parity below this support zone would be in sight again. The skew favoring puts also becomes clear in the following graph:

In this sense, the FX market has priced in the risk of a further fall in the euro somewhat higher. With regard to the ATM options, however, the fear of significantly lower spot level does not seem to be very pronounced at the moment. This could confirm an imminent euro recovery or mean that the market is not well prepared for another slide. This two-way risk makes buying an option outright dangerous. I would rather recommend buying a straddle or a hedged option. The two and three months tenors look the most promising. Protagonists with real dollar needs may be hoping for a recovery rally, which they should use to hedge. The implied volatilities could then trade 25 to 50 points lower.*

Good luck,

Sebbo

(*reminder: my content is intended to be used and must be used for informational purposes only. It is very important to do your own analysis before making any investment based on your own personal circumstances.)