Market update #22

Market update #22

Implied volatilities have fallen significantly once again

The euro is trading less than 25 pips away from the spot level that we observed in the last Market update #21. This almost completely describes the situation on the EURUSD options market. Volatility has disappeared and I am slowly losing faith that it will return in the foreseeable future.

")

The central banks, above all the Fed, have once again managed to put the market to sleep with sufficient liquidity. Although this has certainly saved some US banks, it has particularly pleased equity investors, who have seen almost exclusively green weekly candles since October last year. However, the dampening effect on the capital market as a whole -- CBOE Volatility Index went from 21.27 (27oct23) to 13.85 (today) -- makes it difficult for active FX buy side traders. While directional trades may be good only for a few pips, short-term option buyers are unlikely to have earned the premium even with very active delta hedging.

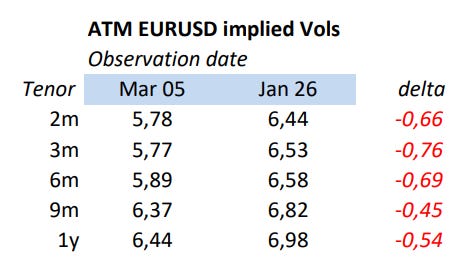

The lower table shows quotes of EURUSD impl vols at 05:30 NY time:

And as usual, here is the comparison with the ATM impl vols at the last observation date:

Implied volatilities have fallen significantly across the entire maturity range and are therefore back at pre-corona levels. One could argue that the 9m and 1y maturities still have room to fall. After all, they are still trading above 6%. However, despite all caution, this is not my base scenario. Players with underlying business should seriously consider whether it is time for hedging transactions. I had already written something similar (albeit with less emphasis) in the last market update. But there are reasons why I always recommend tenors of 3 months or longer for players with a real need to hedge.1 Even someone who bought a 3-month option at the end of January still has a few weeks to look for favourable market developments.

Short-term players looking to profit from rising volatility are keeping an eye on the next market events. This week Friday the NFP figures for February will be published. But when was the last time NFPs were a driver of volatility? I have slightly higher expectations for the CPI numbers next Tuesday. A good week before the FOMC meeting on 20 March, surprisingly high inflation figures in particular could cause a change in risk sentiment. But it is worth remembering that the market has been selling risk almost every day recently. Both CPIs and the FED could therefore become non-events again. This is not my wish, but unfortunately I know very well that it can be expensive to stand up to the market's complacency.2

Good luck,

Sebbo

reminder: my content is intended to be used and must be used for informational purposes only. It is very important to do your own analysis before making any investment based on your own personal circumstances.

After all, FX has the advantage that various determinants influence the price level in both directions. Fortunately, FX can probably never reach the level of complacency of the stock market.