Morning Call #189

Morning Call #189

A deeper look into the Dollar ahead of the CPIs

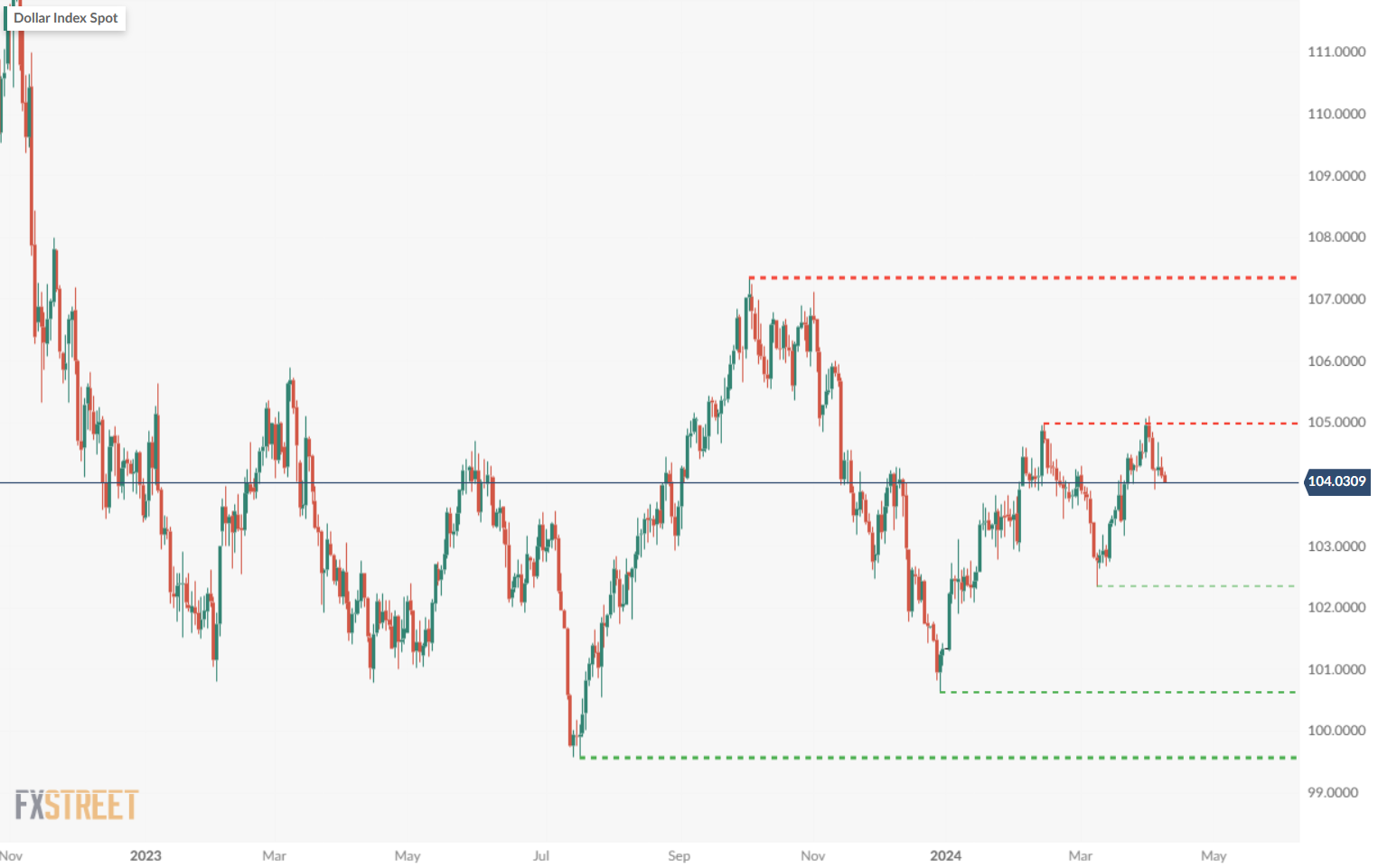

Last week, the key support levels in the XXXUSD crosses held for now (see MC #188). As a result, the dollar index (=DXY) rejected the 105 treshold and formed a double top in the short term picture. Tomorrow, however, the CPI figures for March will be published, which could challenge the bearish dollar case again.

Ultimately, it was the interest rate expectations for 2024 that have put pressure on the dollar index since the beginning of November. Up to seven interest rate cuts were originally expected. Over the last few months, these expectations have been revised to just three rate cuts, and for a few days now, even a year without a single rate cut has been conceivable. The latest published figures on price and wage trends, fairly robust economic data and the recent rise in bond yields support this view. Only the rapid increase in US debt and the sharp rise in financing costs speak against it in some ways. At least that's what the doves are saying. But can Jerome Powell really cut interest rates into a market with ATHs everywhere (stocks, gold, coins), solid economic data and the immense risk of inflation running hotter again?

You will probably lose less money in this market if you do not completely exclude this possibility. In this respect, I definitely do not recommend going all in long dollar.1 I have written many times in recent months that the immense increase in US debt must be accompanied by sufficiently high interest rates to keep the currency attractive. In my view, there is a considerable long-term risk that the dollar carry trades, which have been top performers for several years, will be penalized once the yield/debt ratio reaches a certain (?) level. Of course, this also depends on how the other G10 currencies develop relative to the dollar. After all, the SNB (recently cut interest rates by 25 basis points) and the Riksbank (interest rate cut announced for the next meeting) provided support a few days ago. In this context, it will be also interesting to see what Ms. Lagarde will deliver this Thursday.

In the short and medium term, however, I see a risk that the dollar could test the 2023 highs again. The CPI figures tomorrow could be a trigger if they deviate upwards from analysts' expectations. All in all, there is still a high two-way risk that can only be traded with extreme discipline using directional trades. In this respect, I can only repeat my recommendation to switch to FX options.

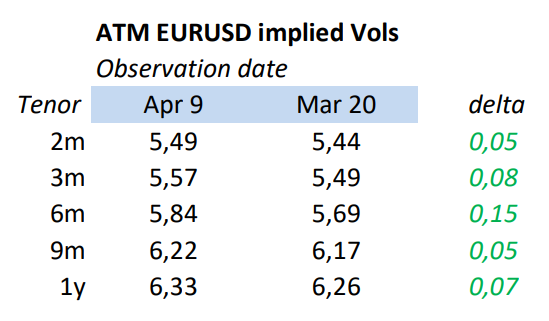

EURUSD implied volatilities, for example, are still trading at a very low level across the entire maturity range.2 This offers short-term investors the opportunity to profit from rising volatility with hedged calls/puts or straddles. Investors with underlying transactions ultimately have to deal with their calculation price. Both dollar buyers and sellers can currently hedge at manageable cost. A 12-month ATM hedge, for example, currently costs around 2.45% of the nominal. However, the ATM strike is 186 pips higher than spot. This probably makes a decision easier for dollar buyers with a calculation rate above the 1.1000 treshold.

Good luck,

Sebbo

reminder: my content is intended to be used and must be used for informational purposes only. It is very important to do your own analysis before making any investment based on your own personal circumstances.

Ultimately, the FX market considers the current vol level to be appropriate. In this respect, “long volatility outright” is also a directional trade, which is accompanied by the risk that implied vols will continue to fall. Please see footnote 1.