Morning Call #144

Yesterday it briefly looked as if the dollar index (DXY) was about to break out of the 100.80/102.20 range. But after a brief high at 102.40, the dollar's "rally" was already over. This confirms our assumption that the range will be resolved after the Fed meeting at the earliest. However, the ECB interest rate decision is also due on Thursday. This could postpone the decision even further. And finally, on Friday, the US NFPs for April will be published.

The weak dollar should ultimately reflect expectations for tonight. Although the market is pricing in another rate hike of 25 basis points to 5.25%, expectations are high that this will finally end the rate hike cycle. On the one hand, this naturally takes the interest rate fantasy out of the dollar, which is driving investors above all else at the moment.

On the other hand, the image that the dollar is losing its reserve status is currently being fed with quite high media intensity (even major serious German news sites are now discovering the topic of "betting against the dollar"). For the BRIC countries, one could certainly agree with this. China has been reducing its dollar-denominated bonds to rock-bottom levels for some years (but is still the second largest creditor of the US after Japan) and geopolitically, the BRIC countries are moving closer together, while tensions with the so-called West are rising.

For other currency areas, however, the picture is less clear. In particular, the dollar index considered here contains only G10 currencies with a particularly high weighting on the euro1:

USDX = 50.14348112 × EURUSD -0.576 × USDJPY 0.136 × GBPUSD -0.119 × USDCAD 0.091 × USDSEK 0.042 × USDCHF 0.036

And especially with regard to the euro, the current dollar (index) weakness may be exaggerated. Given the still high inflation in the eurozone (HICP YoY came in at 7% yesterday), even the expected rate hike of 25 basis points to 3.75% on Thursday is rather a joke.

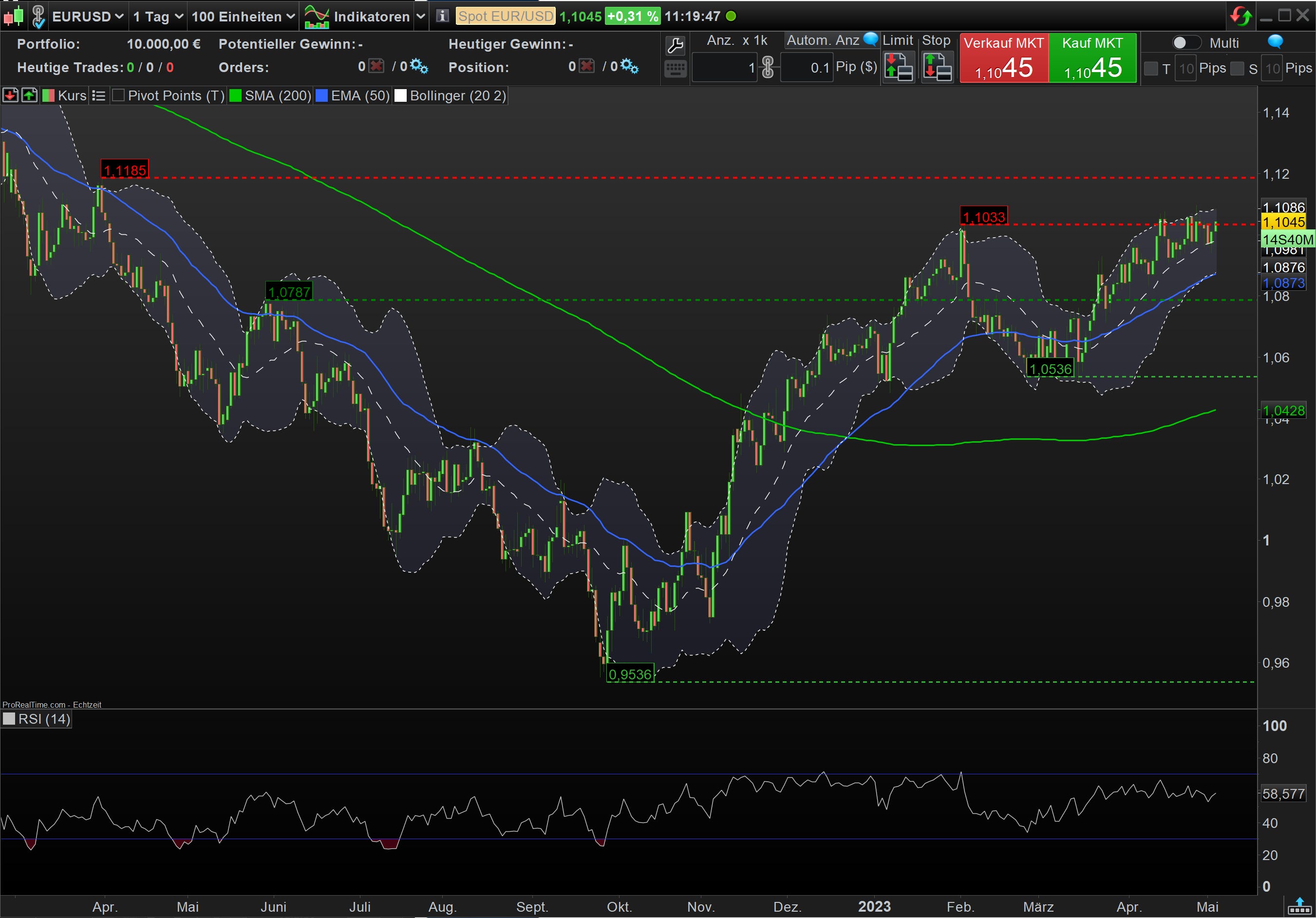

For the time being, I would therefore be cautious with dollar shorts. I can certainly imagine a big first dip in the direction of the 100 mark or below if Powell tonight (euopean) confirms expectations that further interest rate hikes are not on the agenda. However, the sustainability of such a move remains to be seen. The reality check may follow as early as Thursday. In this respect, I would use an equivalent move in the euro towards the 1.1200 to buy dollars.2

Good luck,

Sebbo

This, of course, raises the legitimate question whether another index would not represent reality better (e.g. the annual rebalanced Bloomberg Dollar Spot Index BBDXY). At least for the currencies considered in this newsletter, the problem is still negligible. And the target weights (here for 2021) in the bloomberg index for CNH, KRW and INR were also rather small at 3.00%, 3.43% and 2.96%. Nevertheless, I will think about the topic again.

Reminder: my content is intended to be used and must be used for informational purposes only. It is very important to do your own analysis before making any investment based on your own personal circumstances.